Politics

Ensuring compliance and security in the banking sector

Writer and editor

Updated

Jun 26, 2024

8 min

Millions of us trust banks to safeguard our hard-earned money and personal information. Due to the continuously changing threat scenery, ensuring security requires constant and additional efforts by your bank. Your firm faces the necessary, significant pressure of complying with numerous regulations and laws, and the risk of both financial and reputational harm if it fails to do so.

It’s been reported that in recent years, the United States has seen the highest number of sanctions imposed by various regulatory bodies. From 2008 to 2022, banks in the U.S. paid $37 billion for violations, which makes it the most fined country in the world. Some of these banks include JPMorgan Chase, BNP Paribas, HSBC and Goldman Sachs.

Compliance is important not only for the obvious reasons of protecting your customers’ data and avoiding fines. Also because regulatory frameworks provide a structured roadmap for best practices that promote digital transformation and enhance overall security. Many of these frameworks require a proactive approach to identifying and addressing system weaknesses before cybercriminals can exploit them. As a result, security testing becomes a top preventative method for financial institutions like yours. This article will explain the importance of staying ahead of cyberattacks, the key regulations that influence banks and how managing vulnerabilities ensures compliance.

The challenges faced by banks

Banks face numerous challenges in staying compliant with various cybersecurity regulations and standards. One significant challenge is the complex regulatory environment. Banks operate under a myriad of local and national regulations, each with its own set of cybersecurity requirements. Keeping up with these evolving requirements can be a constant struggle.

Another challenge is the continuous evolution of cyber threats. New vulnerabilities are found all the time, and cybercriminals are constantly developing creative attack methods. These attacks can target not only the banks’ systems but also their suppliers. This makes the attack surface more extensive. It requires banks to be proactive and innovative in their security strategies.

Implementing and maintaining robust cybersecurity measures is another area where banks often struggle. This requires significant resources, including skilled IT personnel, sophisticated technology, ongoing training and knowledgeable attorneys. Small banks may find it challenging to secure the necessary resources to achieve and maintain compliance.

Other challenges include the hybrid work environment and the complexity that remote work brings. Count as well the need for structured and stricter accountability requirements for CEOs and CFOs. Add to that the complexity of regulatory jargon leading to open interpretation. Also, the fast pace of technological advancement that requires banks to regularly update their systems and security measures.

The benefits of compliance

The benefits of compliance go beyond avoiding ample fines. Here are some key motivations to stay compliant:

Better data protection: The primary advantage is privacy protection. By adhering to compliance rules, your bank can significantly mitigate the risk of data breaches. What's more, protecting personal and financial information is crucial for maintaining client trust.

Risk management: Compliance involves identifying, evaluating and managing risks. This enables your bank to proactively counter potential attacks.

Accountability and transparency: Compliance promotes both accountability to regulatory bodies and transparency in banking operations.

Operational efficiency: Proper compliance can lead to smoother operations, as it often involves streamlining processes which improves efficiency.

Competitive advantage: Banks can differentiate themselves in the market as secure and reliable institutions.

Key regulations for banking

As was said above, banks have to navigate a sea of laws and regulations. Each one aims to protect customers from cybersecurity risks by keeping the confidentiality, integrity and availability of financial data and systems. Violations of these regulations can lead to hefty fines, financial losses, reputational damage and increased regulatory surveillance. Below is a breakdown of some key regulations and standards impacting bank cybersecurity:

Payment Card Industry Data Security Standard (PCI DSS): The PCI DSS applies to any organization that handles credit card information. It mandates specific controls for protecting cardholder data, including encryption, access controls and regular security testing.

Regarding the latter, PCI DSS requirement 11: Test Security of Systems and Networks Regularly emphasizes the need for continuous security testing. PCI DSS v4.0.1 mandates internal and external vulnerability scans quarterly and after significant changes, and penetration tests at least annually and after significant changes. Violations can result in increased credit card processing costs, loss of account privileges and even criminal charges, with fines ranging from thousands to millions of dollars depending on the severity of the violation and the presence of data breaches.

We, at Fluid Attacks, have established for our tests these software requirements using this standard.

Gramm-Leach-Bliley Act (GLBA): The GLBA requires financial institutions to protect customers' nonpublic personal information. It mandates the implementation of security measures to protect customer data from breaches and unauthorized access. The act is enforced by bodies such as the Federal Trade Commission (FTC), Federal Deposit Insurance Corporation (FDIC), and others.

As of 2023, GLBA mandates security measures like penetration testing and vulnerability scanning. Its Safeguards Rule requires financial institutions to develop, implement and maintain a comprehensive information security program. Pentesting is required annually, with best practices suggesting more frequent testing. Vulnerability scanning must be performed every six months. Noncompliance can lead to fines of up to $51,744 per violation by the FTC, lawsuits, reputational damage and increased regulatory scrutiny.

Here at Fluid Attacks, we have created for our tests these software requirements based on this law.

New York Department of Financial Services (NYDFS) Cybersecurity Regulation: The NYDFS Cybersecurity Regulation mandates specific cybersecurity controls for financial institutions operating in New York. It includes guidelines for incident response plans, notification requirements in case of breaches, multi-factor authentication and vendor security policies.

23 NYCRR 500 requires annual penetration testing and quarterly vulnerability assessments to identify and mitigate risks. It also mandates continuous monitoring and secure development practices for in-house applications. Noncompliance can result in ample fines, increased inspections and audits, lawsuits and reputational damage.

We established for our tests these software requirements using this regulation.

Bank Secrecy Act (BSA): The BSA focuses on anti-money laundering (AML) and combating financial terrorism (CFT). It requires financial institutions to implement programs to detect and report suspicious activities. While the BSA does not explicitly mandate security testing, it requires robust security measures to ensure the integrity and confidentiality of data used in AML compliance. Regulators that administer BSA, like the Financial Crimes Enforcement Network (FinCEN), do impose requirements that call for security testing.

Fines for willful violations can reach up to $100,000 per violation, with additional consequences including criminal charges, reputational damage, increased oversight and potential revocation of banking licenses.

SWIFT Customer Security Controls Framework: The Society for Worldwide Interbank Financial Telecommunication (SWIFT) provides a global financial messaging system for international transactions. Its Customer Security Program (CSP) and Customer Security Controls Framework (CSCF) outline mandatory and advisory controls to secure local SWIFT environments.

Principle 2 mandates annual vulnerability scanning and remediation documentation, while Principle 7 recommends proactive penetration testing. Noncompliance can increase the risk of cyberattacks and may result in exclusion from the SWIFT network, disrupting international transactions. A notable example is Russia's exclusion from SWIFT due to the European Union's sanctions related to the war against Ukraine.

From our end, we set up for our tests these software requirements using this framework.

Federal Information Security Management Act (FISMA) FISMA requires federal agencies and their contractors, including banks that work with federal systems, to develop, document and implement an information security program. Regular security assessments, continuous monitoring and incident response plans are essential for compliance. Noncompliance can lead to federal contract termination, financial penalties and reputational damage.

We established for our tests these software requirements using this act.

California Consumer Privacy Act (CCPA): CCPA, primarily a data privacy law, impacts cybersecurity practices for banks operating in California. It grants California residents rights over their personal data and imposes requirements on businesses to protect that data. Data protection measures, breach notifications and consumer rights management are essential for compliance. Fines for violations can reach up to $7,500 per intentional violation and $2,500 per unintentional violation, along with potential lawsuits.

These are the software requirements we have set with this act for our tests.

Some useful frameworks for bank compliance

Banks can leverage several cybersecurity frameworks to enhance their security posture and ensure robust protection against cyber threats. Here are some key frameworks whose implementation can be beneficial:

Federal Financial Institutions Examination Council (FFIEC) resources: The FFIEC is an interagency body that provides extensive guidance on cybersecurity and security testing for financial institutions. While the FFIEC does not enforce specific regulations, its guidelines are used by federal banking regulators (such as the FDIC, OCC and Federal Reserve) to evaluate the cybersecurity practices of financial institutions.

National Institute of Standards and Technology (NIST) Cybersecurity Framework: This framework provides guidance for managing cybersecurity risks. Although voluntary, the NIST framework can be a valuable tool for banking institutions to build a comprehensive cybersecurity program. The framework emphasizes identifying vulnerabilities, implementing security controls, continuous monitoring and regular testing.

ISO 27001: This international standard provides structured methods for protecting sensitive data, including financial information, intellectual property, employee information and information entrusted to third parties. A bank's information security management system (ISMS) must be established, implemented, maintained and continuously improved according to the criteria outlined in ISO 27001.

General Data Protection Regulation (GDPR): This European regulation applies for EU banks and non-EU banks that have business with clients in Europe. Its focus is on protecting personal data and ensuring data privacy. This regulation provides excellent examples of the measures banks should implement to safeguard their customers’ information. GDPR requires appropriate technical and organizational measures for financial institutions, therefore helping them build their security posture and fostering excellence in operations.

Recommendations for cybersecurity compliance for banks

Prioritizing a robust cybersecurity posture can be challenging, but with a proactive approach, banks can achieve compliance and in this way create strong security measures in software development. We had previously discussed how banks, and indeed financial institutions in general, should follow best practices to build secure services. But here, we provide some key recommendations to develop secure software applications for banks:

Establish security requirements at the beginning of the SDLC: Using threat modeling early in the development process can help identify potential security risks and create countermeasures.

Integrate secure coding practices throughout development: Secure code review, both manual and automated, can reduce security risks before deployment.

Identify vulnerabilities within the application: Implement static application security testing (SAST) and dynamic application security testing (DAST).

Run vulnerability assessments: Conduct penetration testing and vulnerability scans to identify exploitable weaknesses in the bank’s software system.

Create a vulnerability management strategy: This process involves the identification, evaluation, prioritization and reporting of vulnerabilities throughout various stages of the development cycle to minimize risk exposure.

Implement security controls for third-parties: To ensure the security of software components and libraries, use control measurements, like keeping an updated SBOM. It's also imperative to evaluate the security practices of third-party vendors.

Implement a patch management process: Ensure all software and systems are up-to-date with the latest security patches.

Develop a compliance map: Identify the cybersecurity regulations that apply to your bank, outline the steps required to achieve compliance and continuously review cybersecurity policies.

Document your bank’s cybersecurity policies and procedures clearly: These policies should outline roles and responsibilities, technology used and incident reporting procedures.

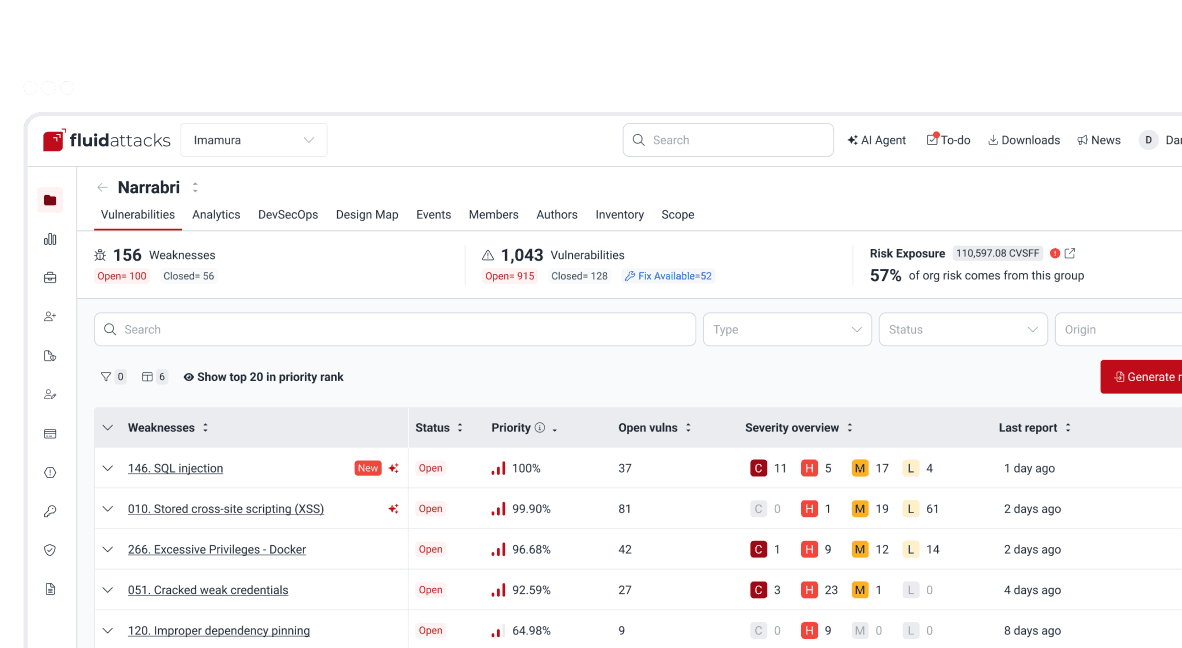

Fluid Attacks offers a comprehensive solution that addresses most of the aforementioned recommendations. Our all-in-one solution aims to identify all vulnerabilities throughout the SDLC and, most importantly, enable their remediation before deployment. Ideal for banks looking to stay compliant, our Continuous Hacking solution helps identify issues and provides detailed reports necessary for accurate management. Our platform has a section to display these details. When integrated with other systems, it offers remediation options that significantly enhance vulnerability management in contrast to when the platform is used only on its own.

We want to help your bank ensure compliance. Contact us now to get started.

Get started with Fluid Attacks' compliance solution right now

Other posts